![JLL Global Hotel Investment Outlook 2026: 22% Growth [Strategy Guide]](https://cdn.sanity.io/images/1la98t0z/production/20eefcf05723840b104648e04a44cd8fd53b2dda-1536x2752.png?w=1920&q=65&auto=format&fit=max)

Key Takeaways

- Global hotel investment is projected to increase by 22% to $72 billion in 2026, driven by strengthening debt markets and consistent travel demand.

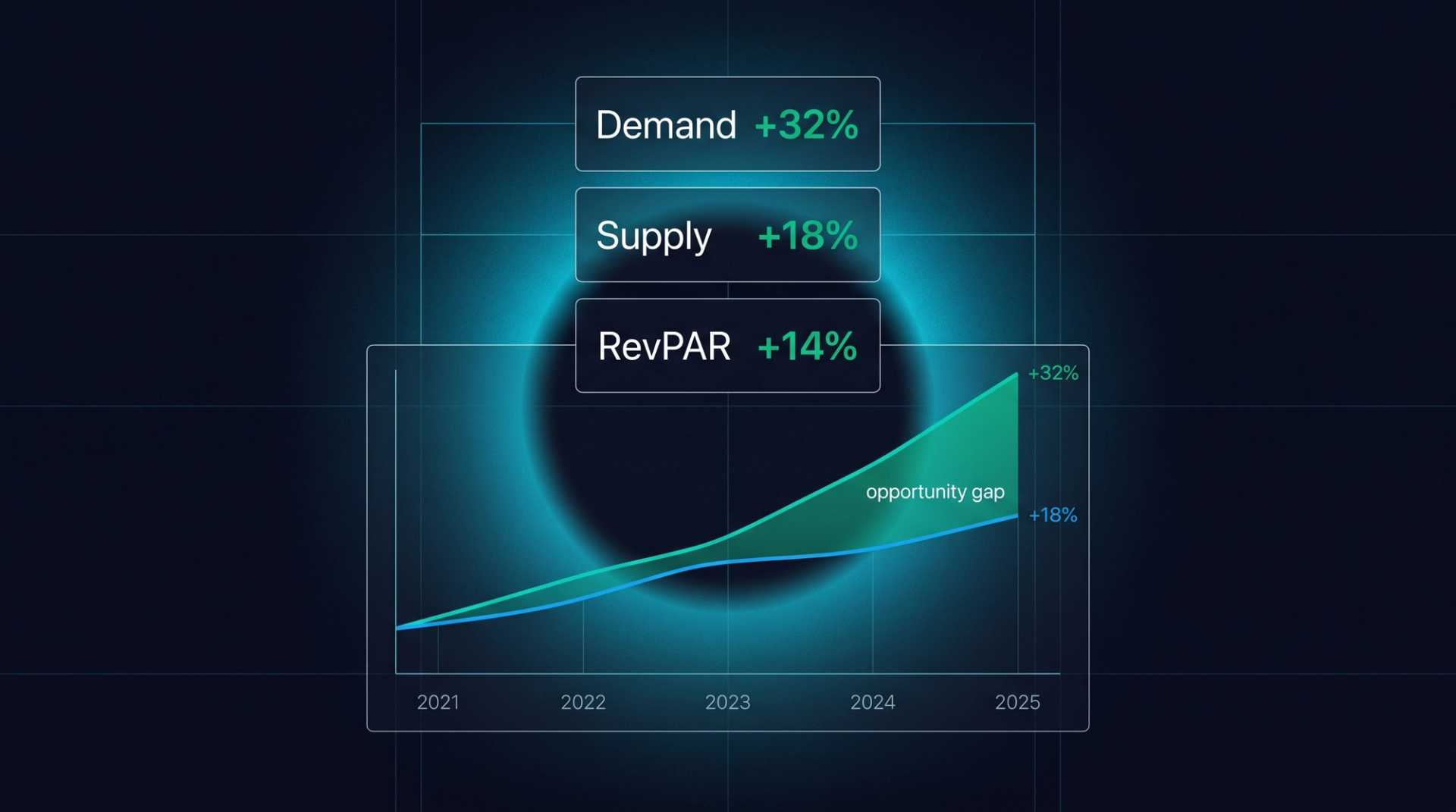

- The luxury hotel segment is identified as the "winning asset class" due to its demand resilience, limited supply, and appealing risk-return profile for investors.

- A significant decline in average hotel loan interest rates (from 7.8% to 5.9%) and increased loan-to-value (LTV) ratios are unlocking previously stalled transactions.

- Turkey's hotel sector, valued at $11.6 billion, is a key investment hotbed with Europe's 3rd largest pipeline (354 hotels), attracting international interest to regions like Bodrum, Cappadocia, and Antalya.

- Investment strategies for 2026 include operational improvement, brand conversion of independent hotels, and new land development in tourism zones.

Global Investment Appetite Rises

JLL's (Jones Lang LaSalle) 2026 Global Hotel Investment Outlook report paints a highly positive picture for the sector. According to the report, global hotel investment volume is expected to increase by 22% in 2026, reaching approximately $72 billion. This growth is driven by strengthening debt markets, falling interest rates, and the structural growth of travel demand.

Hospitality continues to be the fastest-growing asset class among real estate investment categories. Structural issues in the office and retail sectors (remote work, e-commerce) are directing investors towards the lodging sector.

Regional Investment Distribution

| Region | 2025 Volume | 2026 Forecast | Change |

|---|---|---|---|

| Americas | $24.3 billion | $28.7 billion | +18% |

| Europe | €22.1 billion | €27 billion | +22% |

| Asia-Pacific | $11.8 billion | $15.2 billion | +29% |

| Middle East and Africa | $3.1 billion | $4.2 billion | +35% |

The Asia-Pacific region boasts the highest growth rate at 29%. Japan alone attracts 35-40% of the region's investments — driven by a weak yen, high tourism demand, and relatively low pricing. In Europe, a €27 billion volume is supported by strong buyer demand in the luxury and lifestyle segments.

Why Debt Markets Matter

One of the most significant findings of the JLL report is the strengthening of debt markets. Many transactions that did not materialize in 2023-2024 due to high interest rates and credit tightening are now proceeding in 2026.

| Debt Market Indicator | 2024 | 2026 |

|---|---|---|

| Average hotel loan interest (US) | 7.8% | 5.9% |

| Loan-to-value ratio (LTV) | 55% | 65% |

| Loan approval time | 12-16 weeks | 8-10 weeks |

| Active lenders | Limited | Diversified |

The decline in interest rates from 7.8% to 5.9% fundamentally alters investment mathematics. The same hotel generates higher cash flow with lower interest, which increases both acquisition prices and transaction volume.

Luxury Segment: The Winning Asset Class

The JLL report identifies the luxury hotel segment as the winning asset class of 2026. There are three main reasons.

First, demand resilience. During economic fluctuations, luxury travel demand is significantly less affected compared to mid-range and budget segments. In 2025 data, luxury hotels' RevPAR grew at 1.8 times the pace of the overall market.

Second, supply constraint. New luxury hotel construction is limited due to high land costs, long development times, and operational complexity. This preserves the pricing power of existing luxury hotels.

Third, investor appeal. Luxury hotels offer an attractive risk-return profile to institutional investors with higher ADR and lower volatility.

| Segment | 2025 RevPAR Growth | Investor Demand | Supply Increase |

|---|---|---|---|

| Luxury | +9.4% | Very High | Low |

| Upper-midscale | +5.8% | High | Moderate |

| Midscale | +3.2% | Moderate | High |

| Budget | +1.4% | Low | High |

Related reading: 354 New Hotels and 48,396 Beds in Turkey

Turkey: An $11.6 Billion Sector

Turkey's hospitality sector boasts an economic size of $11.6 billion, according to JLL data. Europe's 3rd largest pipeline, 63.9 million tourists, and geographical advantages have placed Turkey on the radar of international hotel investors.

Turkey's investment attraction factors are listed as follows:

| Factor | Detail |

|---|---|

| Tourist volume | 63.9M (4th globally) |

| Pipeline size | 354 hotels (3rd in Europe) |

| Currency advantage | TRY depreciation, high USD-based ROI |

| Luxury potential | Bodrum, Cappadocia, Istanbul |

| Geographical location | Crossroads of Europe-Asia-Middle East |

| Government incentives | Tourism investment zones, VAT reduction |

Bodrum, Cappadocia, Antalya: International Investor Interest

Three Turkish destinations stand out as the regions attracting the most interest from international hotel investors.

Bodrum: The rising star of the Mediterranean in the luxury resort and villa market. Ultra-luxury brands such as Aman, Six Senses, and Mandarin Oriental are already present. New investment interest is concentrated in the branded residences segment. Land scarcity on the Bodrum peninsula helps preserve the value of existing assets.

Cappadocia: Positioned as a unique destination worldwide. The trio of balloon tourism, cave hotels, and cultural experiences provides premium pricing power. Projects from brands like Ritz-Carlton Reserve and Aman are present. As capacity is limited, RevPAR growth potential is high.

Antalya: Beyond the volume market, luxury resort renovation projects in areas like Belek and Kemer are notable. The conversion of older all-inclusive resorts into the luxury segment offers attractive "value creation" opportunities for investors.

Investment Theses and Risk Factors

JLL presents three main theses for 2026 hotel investments:

Thesis 1: Operational improvement. Acquiring underperforming hotels and increasing RevPAR through professional management and revenue management tools. This opportunity is particularly significant in Turkey — many hotels still use Excel-based pricing.

Thesis 2: Brand conversion. Branding independent hotels with international brands. Achieving ADR and occupancy increases through franchise or management agreements. The aggressive growth of IHG and Marriott in Turkey supports this thesis.

Thesis 3: Land development. Developing hotels from scratch in tourism investment zones. Long-term but with the highest return potential. Supported by government incentives.

Risk factors include geopolitical uncertainty, inflationary pressure, and currency volatility. However, JLL states that these risks do not eliminate investment returns but merely increase the risk premium.

Related reading: Revenue Growth in Hotels with Green Certification

Conclusion: Time to Invest

JLL's 2026 report delivers a clear message: global hotel investments are on a strong upward trend, and Turkey is one of the most attractive destinations in this trend. 22% growth, strengthening debt markets, and the dominance of the luxury segment promise strong returns for those who invest in the right projects at the right time.

However, investment success goes beyond selecting the right location and segment; it also depends on professional revenue management. Opening the best hotel in the best location is not enough — systems must be established to maximize revenue from every room night.

Maximize Your Investment Returns with OtelCiro

OtelCiro's revenue management and market analysis platform provides data-driven decision support to hotel investors. Maximize your investment returns with feasibility analysis, market benchmarking, and operational revenue optimization.

Request an investment analysis and explore the opportunities in Turkey's hotel market.

![Europe's Hotel Construction Boom: 2026 Oversupply Risks [Market Analysis]](https://cdn.sanity.io/images/1la98t0z/production/6dfe59137f56aa14bfcba86d9db3cf05ff89f406-2752x1536.jpg?w=1920&q=50&auto=format&fit=max)