![Turkey Hotel Market Analysis 2026: Growth Trends & Data [Data Analysis]](https://cdn.sanity.io/images/1la98t0z/production/e42e6e8bb077bf84bd53548ce07ad4e0c38aa11b-1024x1024.png?w=1920&q=65&auto=format&fit=max)

Key Takeaways

- The Turkish hotel market is projected to reach $48.7 billion by 2026, representing a 27.5% growth since 2023.

- The midscale segment holds the largest market share (45%), while the luxury segment commands the highest ADR at $285.

- Antalya and Istanbul dominate the landscape, collectively accounting for over 50% of total market revenue.

- Hotels utilizing AI-powered revenue reporting tools achieve 23% higher RevPAR compared to those using traditional methods.

- Emerging sectors like health, gastronomy, and digital nomad tourism are expected to drive the market toward a $65 billion valuation by 2030.

Turkey's Hotel Market 2026: Continued Growth

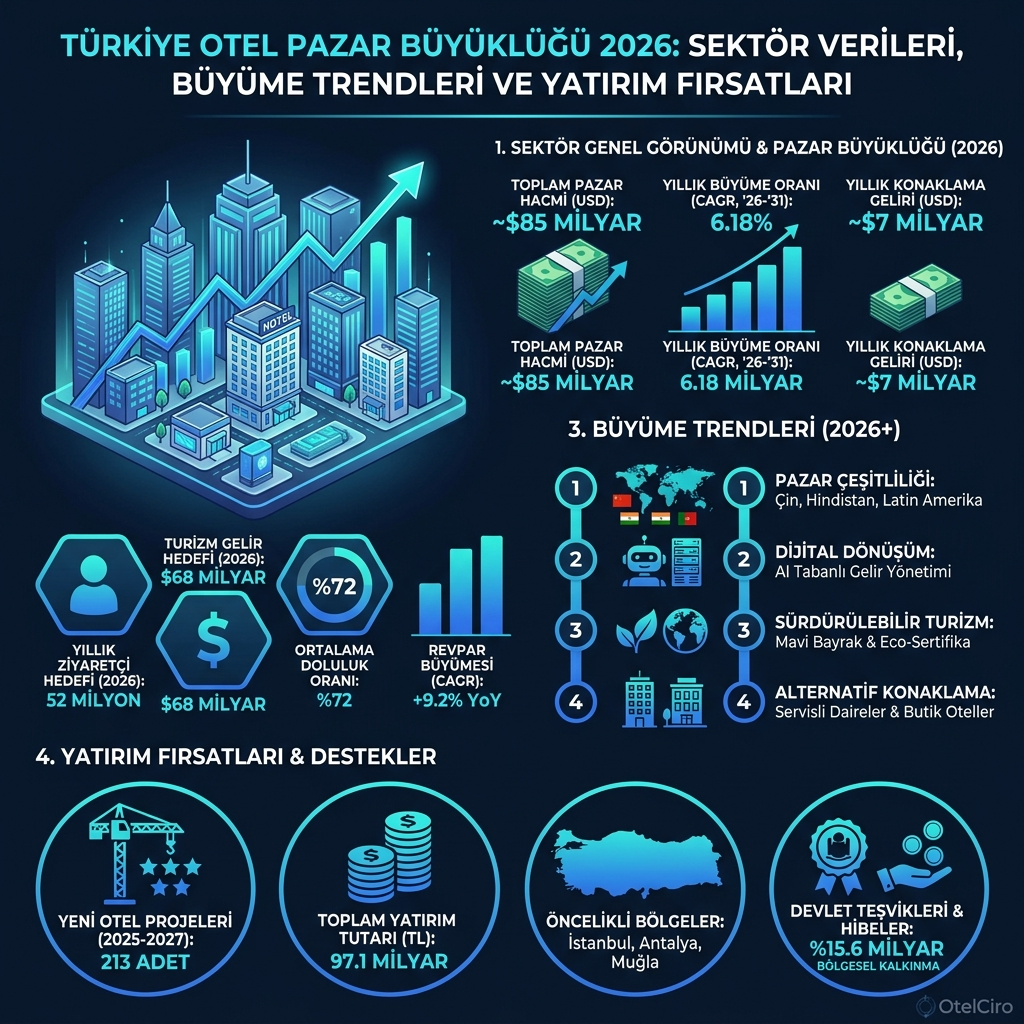

The Turkish hotel market continues to be one of Europe's most dynamic hospitality landscapes, reaching a size of $48.7 billion in 2026. Compared to the $38.2 billion valuation in 2023, the sector has seen a 27.5% growth over three years. This expansion is fueled by both rising domestic tourism demand and a steady increase in international visitor arrivals.

According to data from the Ministry of Culture and Tourism, while the number of tourists visiting Turkey exceeded 62 million in 2025, the 2026 target has been set at 67 million tourists. These figures serve as the primary drivers directly impacting the total market size.

Embed this image on your site

<a href="https://otelciro.com/en/news/turkey-hotel-market-analysis-2026-growth-trends-data-data-analysis">

<img src="https://cdn.sanity.io/images/1la98t0z/production/e42e6e8bb077bf84bd53548ce07ad4e0c38aa11b-1024x1024.png" alt="Turkey Hotel Market Size 2026 Infographic" width="800" />

</a>

<p>Source: <a href="https://otelciro.com">OtelCiro</a> — AI Hotel Revenue Management</p>

Related reading: Hospitality Vision 2026: Trends Shaping the Future of the Industry

Market Analysis by Segment

To accurately understand the Turkish hotel market, it is necessary to evaluate it based on segments. As of 2026, the market distribution is as follows:

Luxury Segment (5-Star and Above)

The luxury accommodation segment accounts for 32% of the total market, valued at $15.6 billion. Istanbul, Antalya, and Bodrum are the main hubs for this segment. While the Average Daily Rate (ADR) in the luxury segment hovers around $285, the occupancy rate remains approximately 72% throughout the year.

New investments by international hotel chains are further strengthening this segment. A total of 14 new luxury hotels are planned to open across Turkey in 2026. Six of these are located in Istanbul, four in the Antalya-Belek region, and two in Bodrum.

Midscale Segment (3-4 Stars)

Representing 45% of the total market, the midscale segment is the largest market slice with a size of $21.9 billion. This segment is supported by both business travel and leisure stays. The ADR average is $95, with an occupancy rate of 68%.

The pace of digitalization in the midscale segment is noteworthy. 61% of hotels in this segment now use at least one AI-based management tool. This rate was only 23% in 2023.

Budget Segment (1-2 Stars and Apartments)

The budget segment makes up 23% of the total market, with a size of $11.2 billion. Driven particularly by increasing domestic tourism demand, the annual growth rate in this segment has reached 18%—the highest growth rate observed among all segments.

Regional Distribution and Concentration

The Turkish hotel market shows significant regional concentration. The distribution based on revenue is as follows:

- Antalya Region: 28% of the total market ($13.6 billion). It remains Europe’s largest resort destination with the all-inclusive concept.

- Istanbul: 24% of the total market ($11.7 billion). High demand persists 12 months a year through both business travel and cultural tourism.

- Aegean Coasts (Muğla-Izmir): 15% of the total market ($7.3 billion). Value is generated through premium boutique hospitality and yacht tourism.

- Cappadocia and Central Anatolia: 8% of the total market ($3.9 billion). A small but profitable market characterized by high ADR.

- Other Regions: 25% of the total market ($12.2 billion). This includes thermal tourism, cultural tourism in the GAP region, and winter sports.

This distribution sends an important message to investors: while the Turkish hotel market seems heavily dependent on Istanbul and Antalya, the growth potential in other regions is much higher. Specifically, annual growth rates of 22-25% are being observed in the Eastern Black Sea and Southeastern Anatolia regions.

Related reading: Antalya Tourism Revenue Analysis: 2026 Trend Report

Investment Opportunities and Return Analysis

As of 2026, the Return on Investment (ROI) in the Turkish hotel market shows significant variation by region and segment:

Highest return investment areas:

- Boutique Hospitality (Cappadocia, Alaçatı): Annual ROI of 14-18%. Profitability is maximized with a low number of rooms but high ADR.

- Urban Hotel Conversion (Istanbul Historic Peninsula): Annual ROI of 12-15%. Restoring historical buildings as hotels offers both cultural value and investment returns.

- Thermal and Wellness Hotels (Afyon, Denizli): Annual ROI of 11-14%. The advantage of year-round occupancy due to health tourism demand.

- Technology-Oriented Management Companies: A low-capital, high-return model via franchise and management agreements.

It has been determined that hotels using AI-supported revenue reporting tools achieve 23% higher RevPAR than hotels working with traditional methods. This difference indicates that technology investment is no longer a choice but a necessity.

Risk Factors and Threats

Like any investment opportunity, the Turkish hotel market carries certain risks:

Macroeconomic Risks: Inflationary pressures and exchange rate fluctuations affect dollar-based returns. In 2026, volatility in the Turkish Lira-USD parity remains the most significant risk factor for international investors.

Oversupply Risk: During the 2024-2026 period, 42,000 new rooms are being added to the market across Turkey. If this supply growth exceeds demand, price pressure may occur, particularly in the midscale segment.

Geopolitical Risks: The geopolitical dynamics of Turkey's geographic location can negatively impact international tourist flows. However, data shows that Turkey's recovery time against geopolitical shocks is steadily shortening—the recovery period, which was 18 months in 2015, has now dropped to 6 months.

Digitalization Lag: 39% of hotels in the market have yet to complete basic digitalization steps. These hotels face the risk of losing their competitive edge.

Future Outlook: 2027-2030 Projections

The Turkish hotel market is expected to reach a size of $65 billion by 2030. The primary drivers of this growth will be:

- Health Tourism: The fastest-growing sub-segment with 25% annual growth.

- Digital Nomad Tourism: Long-term stay demand as the remote work trend becomes permanent.

- Gastronomy Tourism: Driven by the UNESCO Creative Cities Network (Gastronomy) program and the global popularity of Turkish cuisine.

- Sustainable Tourism: Increasing demand for green-certified hotels (GSTC).

In conclusion, the Turkish hotel market offers great opportunities for investors and operators through the right strategy and technology investment. However, to benefit from these opportunities, data-driven decision-making mechanisms and smart revenue management systems have now become an indispensable requirement.

![Europe's Hotel Construction Boom: 2026 Oversupply Risks [Market Analysis]](https://cdn.sanity.io/images/1la98t0z/production/6dfe59137f56aa14bfcba86d9db3cf05ff89f406-2752x1536.jpg?w=1920&q=50&auto=format&fit=max)