Key Takeaways

- Department-based budget planning significantly boosts hotel profitability by an average of 18-24%.

- A successful budget cycle requires a minimum 3-month lead time, starting with comprehensive data collection.

- Leverage AI-powered tools for revenue forecasting (85-92% accuracy) and implement zero-based budgeting to reduce unnecessary expenses by 8-12%.

- Implement monthly variance analysis and flexible budget models to effectively track performance and adapt to market fluctuations.

- Digital budget management tools can shorten the planning process by 40% and increase budget accuracy by 25%.

The New Era in Hotel Budget Planning

The annual budget planning process is one of the most critical management activities, determining a hotel's financial course for the next 12 months. Research conducted in the Turkish hospitality sector indicates that hotels implementing department-based budget planning increase their overall profitability by an average of 18-24%. In contrast, many hotels still operate with a collective budget approach, failing to differentiate departmental performance.

A correct budget planning process encompasses a wide range of activities, from revenue forecasting and cost control to investment planning and cash flow projections. In this guide, we address each step of the department-based budget creation process with practical examples.

Related reading: Hotel Revenue Metrics and KPI Guide

Budget Planning Calendar and Preparation Process

A successful budget planning process should begin at least 3 months in advance. A planning calendar starting in September and concluding by the end of November is considered ideal.

Phase 1: Data Collection (September)

Reliable data forms the foundation of budget planning. The following information must be collected from each department manager:

- Actual data for the last 3 years: Revenue, expenses, occupancy rates, and profit margins

- Current year forecasts: Expected actuals by year-end

- Personnel plans: Staffing needs, promotion, and salary increase requests

- Investment requests: Equipment renewal, technology updates, renovations

Phase 2: Revenue Forecasting (October)

Revenue forecasting constitutes the backbone of the budget. Separate revenue projections should be prepared for each department:

- Rooms department: Calculated by occupancy rate x ADR x number of rooms x days

- Food & Beverage: Guest spending per person x expected number of guests

- Spa & Wellness: Capacity utilization rate x average transaction amount

- Meetings & Events: Room rental revenues + F&B component

AI-powered forecasting tools can generate revenue projections with an 85-92% accuracy rate by analyzing market trends and macroeconomic indicators alongside historical data.

Phase 3: Expense Planning (October-November)

The expense budget begins with the segregation of fixed and variable costs:

Fixed costs: Rent, insurance, depreciation, core personnel expenses Variable costs: Energy, materials, additional personnel, commissions Semi-variable costs: Maintenance, marketing, training

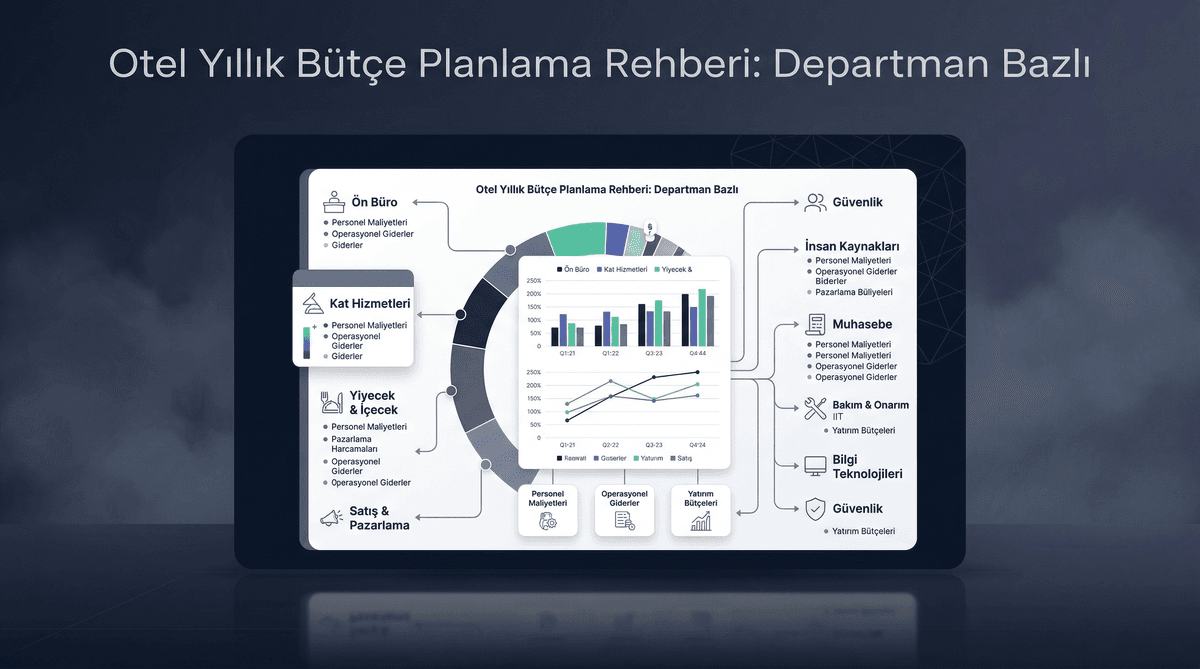

Department-Based Budget Structure

Rooms Department Budget

The rooms department typically generates 55-70% of total revenue in most hotels and has the highest profit margin. This department's budget includes the following items:

| Revenue/Expense Item | Percentage of Total Revenue |

|---|---|

| Room revenues | %55-70 |

| Front desk personnel | %4-6 |

| Housekeeping personnel | %5-8 |

| Housekeeping supplies | %2-3 |

| Room amenities | %1-2 |

| Laundry | %2-3 |

| Department profit margin | %70-80 |

Food & Beverage Department Budget

The F&B department usually accounts for 25-35% of total revenue, but its profit margin is lower compared to the rooms department. Food costs should be targeted at 28-35% of revenue, while beverage costs should be around 20-25%.

Critical control points:

- Food cost ratio: Monitored through monthly inventory counts

- Portion control: Standard recipe costing

- Waste management: Minimized with daily production planning

- Menu engineering: High-margin products highlighted

Spa & Wellness Budget

The spa department typically requires 45-55% capacity utilization to reach its break-even point. Therapist costs constitute the largest expense item in the department's budget, representing 35-45% of total revenue.

Related reading: Department-Based Profit Margin Analysis

Cost Control Mechanisms

Monthly Variance Analysis

Monitoring budget-to-actual variance on a monthly basis is critical for early detection of deviations. Each department manager should submit an explanation report if there is a deviation of more than 5% from the budget.

Effective variance analysis should be three-dimensional:

- Volume variance: The difference between expected and actual demand

- Price variance: The difference between planned and actual prices

- Cost variance: The difference between budgeted and actual expenses

Zero-Based Budgeting Approach

Traditional budgeting involves adding a certain increase to the previous year's figures. However, zero-based budgeting requires justifying every expense item from scratch. Hotels implementing this approach successfully reduce unnecessary expenses by an average of 8-12%.

Flexible Budget Model

Fluctuations in occupancy rates are inevitable in the hospitality industry. A flexible budget model defines separate expense budgets for different occupancy scenarios (50%, 65%, 80%, 90%), enabling realistic performance measurement.

Budget Tracking with Technology

Digital tools significantly simplify the budget planning process. OtelCiro's reporting module provides real-time, department-based budget-to-actual comparisons.

Advantages offered by modern budget management systems:

- Real-time tracking: Instant monitoring of daily revenue and expense flows

- Automated alerts: Immediate notifications for budget overruns

- Scenario analysis: Financial impact of different occupancy and pricing scenarios

- Forecast updates: Automatic revision of year-end forecasts based on actuals

According to research, hotels using digital budget management tools shorten the planning process by 40% while increasing budget accuracy by 25%.

Capital Expenditure (CapEx) Planning

The capital expenditure (CapEx) budget, an integral part of the annual budget, covers a hotel's physical infrastructure and technology investments. As a general rule, 4-6% of total revenue should be allocated to annual maintenance and renovation investments.

ROI (Return on Investment) analysis should be the basis for prioritizing investments:

- High ROI: Energy efficiency investments (2-3 year payback)

- Medium ROI: Technology investments (3-5 year payback)

- Long-term ROI: Renovation and expansion (5-8 year payback)

Conclusion: A Data-Driven Budget Culture

Department-based budget planning is a strategic tool that strengthens a hotel's financial discipline and fosters accountability for every manager. A successful budgeting process not only accurately forecasts figures but also enhances operational efficiency, rationalizes investment decisions, and forms the foundation for a long-term growth strategy.

Do you want to digitalize your hotel's budget planning process and transition to department-based performance tracking? Contact us for a free demo.

![US Hotel Labor Costs Hit $131 Billion in 2026: AI Automation Strategies That Cut Costs Fast [2026 Guide]](https://cdn.sanity.io/images/1la98t0z/production/6765e31b08a1c04cce66f9bf9482693dbefdcce5-2752x1536.jpg?w=1920&q=50&auto=format&fit=max)