The Scale of Hilton's India Commitment

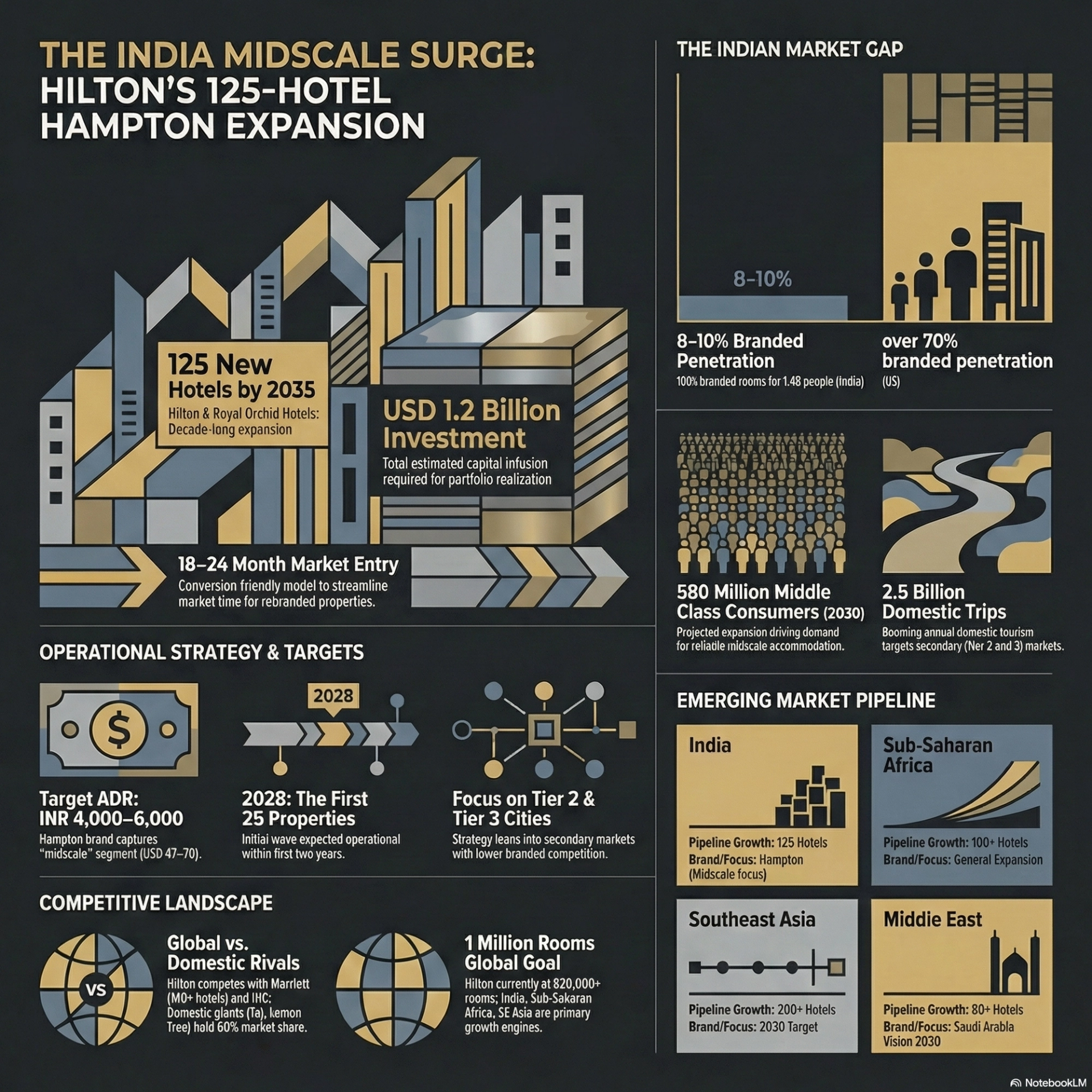

In early 2026, Hilton Worldwide confirmed one of the most ambitious hotel expansion plans in the company's 105-year history: 125 Hampton by Hilton properties across India, with the bulk of openings targeted between 2027 and 2035. This is not an aspirational pipeline number — it is backed by signed agreements with Indian development partners and a dedicated regional development team based in Gurugram.

To understand the magnitude: Hilton currently operates approximately 45 hotels across all brands in India. The Hampton rollout alone would nearly triple the company's Indian footprint. Combined with planned openings under the Hilton Garden Inn, DoubleTree, and Conrad brands, Hilton's total India portfolio could exceed 200 properties by 2035.

Why India, Why Now

The Accommodation Deficit

India welcomed approximately 19 million international tourists in 2025 and over 2.5 billion domestic trips — yet the country has only an estimated 150,000-180,000 branded hotel rooms. For comparison, the United States has approximately 5.7 million hotel rooms serving 350 million residents. India's 1.4 billion people are served by roughly 3% of that capacity.

The math creates a structural opportunity: India needs an estimated 300,000-400,000 additional branded hotel rooms over the next decade to meet projected domestic and international travel demand. This shortage is most acute outside the major metro areas — precisely where Hampton by Hilton's mid-market positioning excels.

Rising Middle Class Travel

India's middle class — households earning $12,000-50,000 annually — is projected to grow from approximately 350 million people in 2025 to 500 million by 2030. This demographic is driving a surge in domestic travel that overwhelmingly favors branded, reliable accommodation in the $50-90 per night range.

Hampton by Hilton's global positioning sits squarely in this sweet spot. The brand's promise of clean rooms, free breakfast, and consistent quality at a mid-market price point mirrors exactly what India's emerging travel class demands.

Government Infrastructure Investment

India's hospitality expansion is supported by massive infrastructure investment:

- Airports: 21 new greenfield airports under construction or planned through 2030

- Highways: The Bharatmala Pariyojana project is building 65,000+ km of highways connecting Tier 2 and Tier 3 cities

- Railways: The Vande Bharat high-speed rail network is making 4-6 hour intercity trips practical for business travelers

- Digital payments: UPI processed 14.6 billion transactions in December 2025 alone, making branded hotel booking frictionless even in smaller cities

Each infrastructure project opens new markets that were previously inaccessible to branded hotel chains.

The Geographic Strategy

Hilton's India expansion is deliberately focused on western and southern regions, with a calculated approach to city selection:

Priority Markets

| Region | Target Cities | Rationale |

|---|---|---|

| Western India | Mumbai suburbs, Pune, Ahmedabad, Surat, Nashik, Vadodara | Industrial corridor, Gujarat growth, IT hubs |

| Southern India | Bengaluru satellites, Hyderabad, Chennai, Coimbatore, Kochi, Vizag | Technology sector, medical tourism, manufacturing |

| Northern India | Delhi NCR expansion, Jaipur, Lucknow, Chandigarh, Amritsar | Government, heritage tourism, education |

| Central/East | Indore, Bhopal, Bhubaneswar, Ranchi | Emerging economic centers, underserved markets |

The emphasis on western and southern India reflects where corporate travel demand is growing fastest. Bengaluru, Hyderabad, and Pune collectively account for over 60% of India's technology sector employment, driving consistent Monday-through-Thursday business travel demand — the bread and butter of mid-market hotel profitability.

The Tier 2/3 City Play

Perhaps the most strategically significant aspect of Hilton's plan is its explicit focus on Tier 2 and Tier 3 cities. While competitors concentrate on Delhi, Mumbai, and Bengaluru, Hilton is targeting cities like Surat (population 7.5 million, GDP growth 9%+), Vizag (major port and IT hub), and Coimbatore (manufacturing and education center).

These markets share several characteristics that favor Hampton's model:

- Limited branded competition: Often fewer than 5 branded hotels in the entire city

- Strong domestic demand: Business and family travel that is underserved by current supply

- Lower land and construction costs: Enabling faster developer returns

- Growing air connectivity: New airports and routes making these cities accessible

Hilton's Africa Parallel

The India expansion does not exist in isolation. Simultaneously, Hilton has announced plans to expand to 180 hotels across Africa — up from approximately 80 currently — creating over 20,000 direct jobs across the continent.

Key African markets include:

- Nigeria: Lagos and Abuja remain priority markets, with expansion into Port Harcourt and Kano

- Kenya: Nairobi as the East African hub, with beach resort properties along the coast

- Egypt: Cairo, Alexandria, and Red Sea resort markets

- Morocco: Casablanca, Marrakech, and Tangier benefiting from tourism growth

- South Africa: Johannesburg, Cape Town, and Durban with business and leisure positioning

The African expansion mirrors the India strategy: targeting emerging markets with structural accommodation deficits, rising middle classes, and improving infrastructure. Hilton estimates the African hotel market will require 500,000+ additional branded rooms by 2035 to meet demand.

What This Means for Global Hospitality

Hilton's twin expansion announcements signal several important shifts for the broader industry:

1. The Center of Gravity Is Moving

For decades, hotel industry growth was synonymous with the US, Europe, and China. Hilton's commitment to India and Africa reflects a recognition that the next wave of hospitality growth is in South Asia, Southeast Asia, and Sub-Saharan Africa — markets with young populations, rising incomes, and massive accommodation deficits.

This has implications for every hotel company. Brands that are not developing their emerging market strategies now will find themselves playing catch-up against first movers with established distribution, loyalty member bases, and developer relationships.

2. Mid-Market Is the Growth Engine

Hilton chose Hampton — not Conrad, not Waldorf Astoria — as the vehicle for its India expansion. This is a deliberate bet that the highest-volume growth opportunity globally is in the $50-100 per night segment, not luxury. Marriott's expansion of Fairfield and Four Points in similar markets confirms this thesis.

For independent hoteliers in emerging markets, this means increased competition at the mid-market level. The response must be either differentiation (unique local experience that a Hampton cannot replicate) or operational excellence (matching branded consistency and distribution reach through technology).

3. Franchise-Light Models Will Dominate

Hilton's India expansion relies primarily on management contracts and franchise agreements rather than owned properties. This asset-light approach allows rapid scaling with limited capital risk. The company targets development partners who bring local market knowledge, land access, and construction capabilities while Hilton provides brand standards, distribution systems, and loyalty programme integration.

This model is being replicated across emerging markets and is particularly relevant for independent hotel operators considering brand affiliation. The value proposition of a global brand — distribution reach, loyalty traffic, revenue management systems — becomes more compelling as markets develop and travelers become more brand-aware.

4. Revenue Management Complexity Increases

As branded supply grows in emerging markets, revenue management sophistication must follow. Markets that previously operated on simple seasonal pricing will need:

- Dynamic pricing responsive to real-time demand signals

- Channel management across OTAs, brand.com, and corporate channels

- Competitive intelligence as new properties enter the market

- Demand forecasting that accounts for infrastructure-driven demand shifts (new airport routes, highway openings, convention centers)

The Competitive Response

Hilton is not alone in targeting India and Africa. The competitive landscape is intensifying:

| Brand | India Pipeline (Rooms) | Africa Pipeline (Rooms) |

|---|---|---|

| Marriott International | 18,000+ | 12,000+ |

| Hilton Worldwide | 15,000+ (Hampton-led) | 10,000+ |

| IHG Hotels & Resorts | 12,000+ | 8,000+ |

| Accor | 8,000+ | 15,000+ |

| Wyndham Hotels | 10,000+ | 5,000+ |

The combined pipeline suggests 60,000+ branded rooms entering the Indian market over the next decade — a transformational increase that will reshape competitive dynamics, rate structures, and distribution patterns.

Implications for Revenue Strategy

For hotel operators worldwide, Hilton's expansion carries actionable implications:

If you operate in India or Africa: The arrival of major branded competition means the window for operating with basic revenue management practices is closing. Invest in technology — dynamic pricing, channel management, and competitive intelligence — before branded properties open in your market and immediately capture the most profitable demand segments.

If you operate in mature markets: Watch for demand displacement effects. As branded hotels make emerging market destinations more accessible and reliable, some leisure and business demand may shift from traditional European and North American destinations to India, Africa, and Southeast Asia. Adjust your source market analysis accordingly.

If you are evaluating brand affiliation: Hilton's willingness to deploy Hampton at scale in emerging markets signals strong confidence in the mid-market franchise model. The economics of brand affiliation — particularly access to Hilton Honors' 190+ million members — become more compelling as these markets mature.

Strategic Takeaway

Hilton's 125-hotel bet on India and 180-hotel expansion in Africa are not just corporate growth stories — they are leading indicators of where global hospitality demand is heading for the next decade. The markets with the most significant accommodation deficits, the fastest-growing middle classes, and the most aggressive infrastructure investment will define the industry's growth trajectory. For revenue managers and hotel operators everywhere, the message is clear: the future of hospitality is being built outside the traditional core markets, and your strategy needs to account for that shift.

![Hilton AI Planner: The Hotel AI Arms Race [2026]](https://cdn.sanity.io/images/1la98t0z/production/68d57604b4e1fdcb0fd2bdc641a6507a7edddd01-1200x1200.png?w=1920&q=50&auto=format&fit=max)

![Middle East Crisis: Turkey's Hotel Opportunity [2026]](https://cdn.sanity.io/images/1la98t0z/production/3c8cd1f63bba930eea22799e7e9de638fa451297-1200x1200.png?w=1920&q=50&auto=format&fit=max)